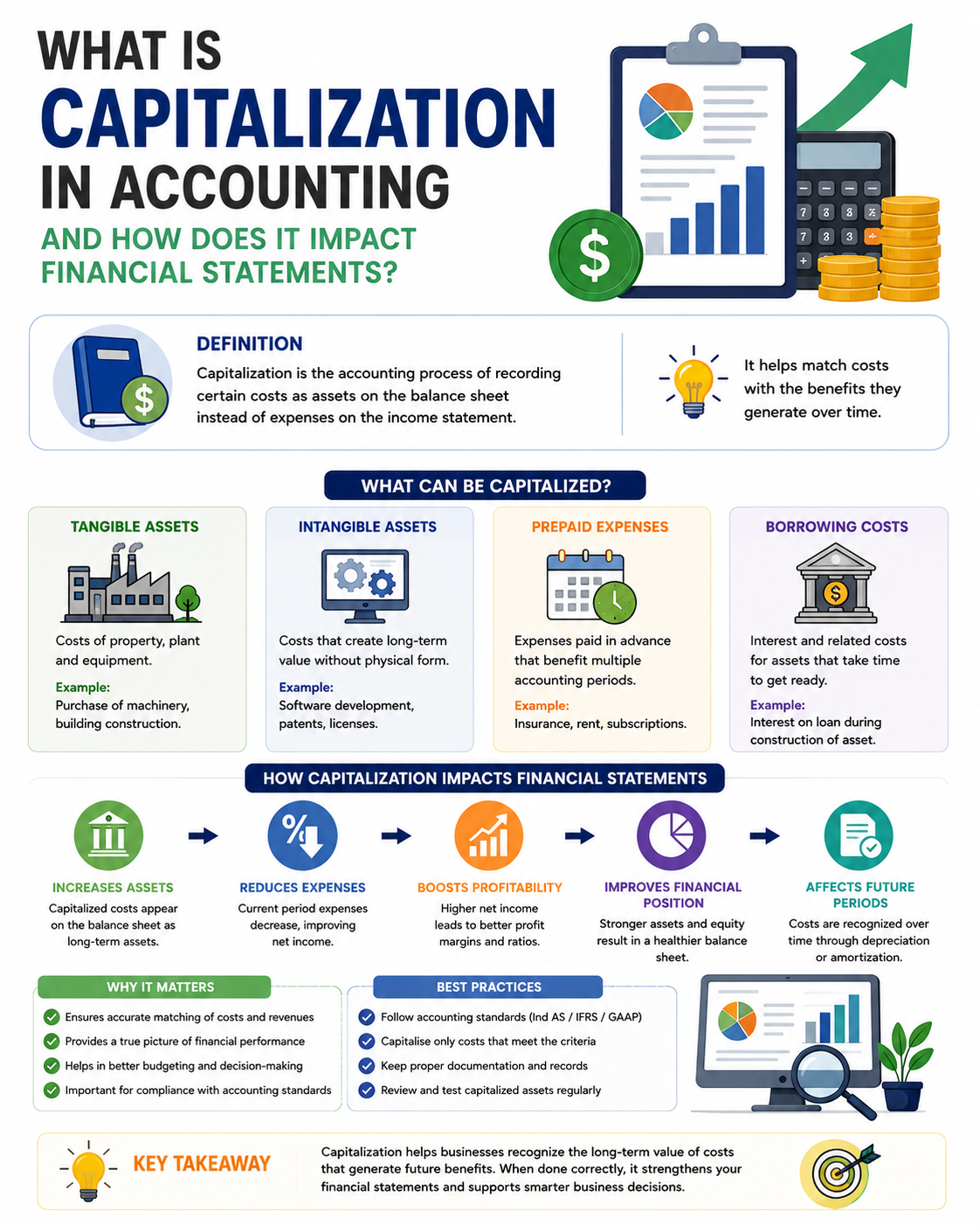

If you've ever bought expensive equipment, renovated your office, or purchased software for your business, you've faced one of the most important decisions in accounting: Should this cost be recorded as an expense or an asset? That decision is called capitalization — and getting it wrong can mean misstated financials, IRS penalties, and a distorted picture of your business's true financial health.

If you've ever bought expensive equipment, renovated your office, or purchased software for your business, you've faced one of the most important decisions in accounting: Should this cost be recorded as an expense or an asset? That decision is called capitalization — and getting it wrong can mean misstated financials, IRS penalties, and a distorted picture of your business's true financial health. Whether you're a business owner, bookkeeper, or finance professional, understanding capitalization in accounting is not optional. It affects your balance sheet, income statement, and cash flow statement simultaneously — and it has major implications for your taxes.

How Capitalization Impacts Financial Statements

Capitalization doesn't just change one number on one statement — it ripples through all three major financial statements simultaneously.

Impact on the Balance Sheet

When you capitalize a cost, it appears as an asset under Property, Plant & Equipment (PP&E) or Intangible Assets. Total assets increase. As the asset is depreciated over time, accumulated depreciation reduces the net book value. A higher asset base improves certain financial ratios that lenders and investors watch closely, like return on assets and debt-to-equity.

Impact on the Income Statement

Only the annual depreciation expense hits the income statement each period — not the full cost. This means your net income is higher in the year of purchase compared to if you had expensed the full amount. In future years, the depreciation charge reduces profit incrementally. Over the asset's full life, the total cost recognized is identical — it's only the timing that changes.

Impact on the Cash Flow Statement

Capital expenditures appear as investing activities on the cash flow statement, not operating activities. This means when you capitalize a cost, operating cash flow looks stronger because the full cash outflow isn't deducted from operations. This is why investors and analysts look at both operating cash flow and free cash flow (which subtracts capex) when evaluating a business.

Side-by-Side Financial Impact Example

Imagine your business spends $60,000 on equipment with a 5-year useful life. Here's how the two approaches compare in Year 1:

| Metric | Capitalize | Expense |

|---|---|---|

| Revenue | $300,000 | $300,000 |

| Cost recognized (Year 1) | $12,000 (depreciation) | $60,000 (full amount) |

| Net Income | $138,000 | $90,000 |

| Total Assets | +$48,000 (net book value) | $0 added |

| Operating Cash Flow | Stronger | Weaker |

| Tax deduction (Year 1) | $12,000 only | $60,000 |

The choice matters enormously — especially when your financials are being reviewed by a bank, investor, or potential buyer.

Capitalization and Depreciation: How They Work Together

Once you capitalize an asset, you must systematically spread that cost over its useful life through depreciation or amortization. The most common methods include:

Straight-Line Depreciation — Equal annual expense over the useful life. ($60,000 ÷ 5 years = $12,000/year). Simplest and most widely used.

Double Declining Balance — Higher depreciation in early years, tapering off later. Best for assets that lose value quickly, like vehicles and technology.

Units of Production — Depreciation based on actual usage or output. Best for manufacturing equipment where wear depends on production volume.

MACRS (Modified Accelerated Cost Recovery System) — The IRS-mandated method for tax returns. Assigns assets to specific recovery periods (5-year, 7-year, 15-year, etc.).

Section 179 / Bonus Depreciation — Allows full deduction of qualifying assets in Year 1 for tax purposes, even if the asset is capitalized on your financial statements. This is one of the most powerful tax strategies available to small businesses.

Setting Your Capitalization Threshold

Every business needs a written capitalization policy that defines the minimum cost an item must reach before it's capitalized rather than expensed. Without one, your accounting is inconsistent — and the IRS will notice.

Step 1: Choose your threshold. Most small businesses use $500–$2,500. The IRS safe harbor is $2,500 per item without audited financials, and $5,000 with them.

Step 2: Write it into a formal accounting policy document. The IRS Tangible Property Regulations (effective since 2014) require businesses to have and consistently follow a written capitalization policy.

Step 3: Apply it consistently every single accounting period. Changing thresholds frequently is a red flag to auditors.

Step 4: If you're changing your existing capitalization method, you may need to file IRS Form 3115 (Application for Change in Accounting Method).

Common Capitalization Mistakes That Trigger IRS Problems

Mistake 1: Expensing costs that should be capitalized.

Some businesses expense major improvements to avoid depreciation complexity. This understates assets, overstates expenses, and can trigger IRS questions when your expense-to-revenue ratio looks abnormally high.

Mistake 2: Capitalizing costs that should be expensed.

Aggressively capitalizing routine costs inflates your asset base and overstates profitability — which lenders, auditors, and the IRS are trained to spot.

Mistake 3: Forgetting to include all acquisition costs.

The capitalized cost includes more than just the purchase price. Shipping, installation, testing, legal fees, and site preparation are often part of the cost basis and must be capitalized alongside the asset itself.

Mistake 4: No written capitalization policy.

Without a documented, consistently applied policy, your capitalization decisions look arbitrary and won't hold up under audit.

Mistake 5: Misclassifying repairs as improvements (or vice versa).

This is one of the most common IRS audit triggers for small businesses. Your CPA should review all major repair and maintenance decisions before you record them.

Frequently Asked Questions About Capitalization in Accounting

What is the capitalization threshold in accounting?

The capitalization threshold is the minimum cost an asset must exceed to be recorded on the balance sheet rather than expensed immediately. For small businesses, the IRS safe harbor is $2,500 per item. Businesses with audited financial statements can use a $5,000 threshold. Your policy must be documented in writing and applied consistently.

Can you capitalize labor costs?

Yes, in certain situations. If employees or contractors spend time constructing an asset — such as building custom software or a facility — those labor costs may be capitalized as part of the asset's cost. Day-to-day operational labor is always expensed.

Is software capitalized or expensed?

It depends on the type. Purchased off-the-shelf software is generally capitalized and amortized. Internally developed software is expensed during the preliminary stage, capitalized during the application development stage, and expensed again during post-implementation. Monthly SaaS subscriptions are expensed as incurred.

How does capitalization affect taxes?

Capitalizing an asset means you deduct the cost gradually through depreciation rather than all at once. However, Section 179 and Bonus Depreciation allow full deduction in Year 1 for tax purposes — even if the asset is capitalized on your books. This is one of the most powerful tax planning tools available to business owners.

What happens if you incorrectly capitalize or expense a cost?

Incorrect capitalization leads to misstated financial statements. Depending on the size of the error, you may need to restate prior-period financials. From a tax standpoint, incorrect deductions can result in IRS penalties, back taxes, and interest charges.

Final Takeaway

Capitalization in accounting is far more than a bookkeeping technicality — it's a decision that shapes how profitable your business appears, how strong your balance sheet looks, and how much tax you owe each year.

The core principle is simple: costs that benefit your business beyond one year belong on the balance sheet as assets, not on the income statement as expenses. But the application requires judgment, written policies, and a solid understanding of GAAP and IRS rules.

If you're unsure whether a cost should be capitalized or expensed — or if you want to review your current capitalization policy — speaking with a CPA before recording the transaction is always the right move. One wrong classification can ripple through your financials for years.