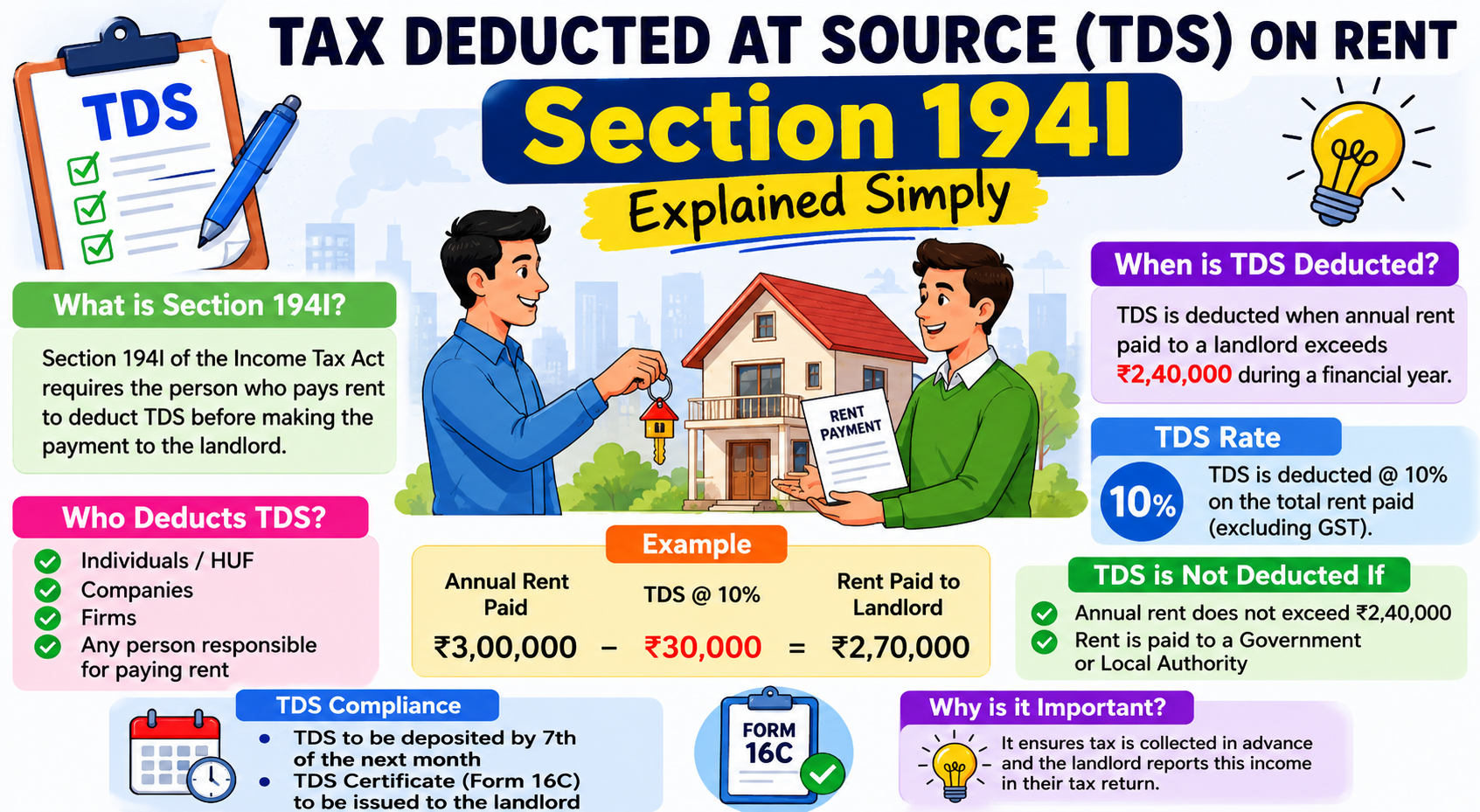

If you pay rent for office space, a shop, a warehouse, or even machinery — and your payments cross a certain threshold — the Income Tax Act requires you to deduct tax before making the payment. This is called TDS on rent, and it is governed by Section 194I of the Income Tax Act, 1961. Many tenants — especially small business owners and professionals — are unaware of this obligation. They pay rent in full without deducting TDS, only to receive a notice from the Income Tax Department later for non-compliance.

What Is TDS on Rent?

TDS (Tax Deducted at Source) is a mechanism where the person making a payment deducts a portion of it as tax and deposits it directly with the government — on behalf of the recipient.

Under Section 194I, any person (other than individuals and HUFs not subject to tax audit) paying rent above the specified threshold must deduct TDS at the time of payment or credit — whichever is earlier.

The logic is simple: instead of waiting for the landlord to declare rental income and pay tax on it at year-end, the government collects the tax upfront through the tenant.

Who Must Deduct TDS Under Section 194I?

TDS under Section 194I must be deducted by:

- Companies (private limited, public limited, LLPs)

- Partnership firms

- Individuals and HUFs whose accounts are subject to tax audit under Section 44AB in the preceding financial year

Who is exempt from deducting TDS on rent?

- Individuals and HUFs whose accounts are not required to be audited — i.e., those whose business turnover is below the tax audit threshold (₹1 crore for business, ₹50 lakh for profession under normal provisions)

- Government tenants paying rent to government landlords (in certain cases)

Note: Even if an individual is exempt from Section 194I, they may still be required to deduct TDS at 5% under Section 194IB if they pay monthly rent exceeding ₹50,000. Section 194IB is a separate provision specifically for individual and HUF tenants — covered below.

What Is the Threshold Limit Under Section 194I?

TDS under Section 194I is applicable only if the annual rent payable to a single landlord exceeds ₹2,40,000 in a financial year.

If the total rent paid or payable during the year is ₹2,40,000 or less, no TDS needs to be deducted.

Example:

- Monthly rent = ₹18,000 → Annual rent = ₹2,16,000 → No TDS required

- Monthly rent = ₹22,000 → Annual rent = ₹2,64,000 → TDS must be deducted

The threshold is assessed per landlord — not per property. If you rent two properties from the same landlord, the combined rent is considered.

TDS Rates Under Section 194I

The rate of TDS depends on what type of asset is being rented:

| Type of Asset Rented | TDS Rate |

|---|---|

| Land | 10% |

| Building (commercial or residential) | 10% |

| Furniture and fittings (let along with building) | 10% |

| Plant and machinery | 2% |

| Equipment | 2% |

| Machinery rented separately (not with building) | 2% |

Key points on rates:

- If the landlord does not provide their PAN, TDS must be deducted at 20% (the higher rate under Section 206AA)

- The 10% rate applies to land, building, and furniture — all at the same rate if rented together

- Machinery and equipment attract only 2% because they are productive assets and the government wants to encourage their use

What Exactly Counts as "Rent" Under Section 194I?

Section 194I defines rent broadly. It includes any payment made under any lease, sub-lease, tenancy, or any other agreement or arrangement for the use of:

- Land

- Building (including factory buildings)

- Land appurtenant to a building

- Machinery

- Plant and equipment

- Furniture and fittings

Whether the payee owns the asset or not — it still qualifies as rent for TDS purposes.

What is NOT covered under Section 194I?

- Hotel accommodation charges — these are typically treated as payment for services, not rent

- Warehouse charges where the warehouseman has control over the goods (treated as service charges, not rent)

- Lease premium paid as a one-time upfront payment (may be treated differently)

- Advance rent that is adjustable against future rent — TDS applies when the advance is credited or paid, not when adjusted

When Must TDS Be Deducted?

TDS under Section 194I must be deducted at the time of:

- Credit of rent to the landlord's account, or

- Actual payment of rent (by cash, cheque, NEFT, etc.)

Whichever happens earlier.

In practice, most businesses credit rent monthly in their accounts. TDS should be deducted at that point — even if the actual cash payment happens later.

If rent is credited in advance for the full year (e.g., in April for the entire financial year), TDS must be deducted on the full amount at that time.

When Must TDS Be Deposited With the Government?

After deducting TDS, the tenant must deposit it with the government within the prescribed due dates:

| Month of Deduction | Due Date for Deposit |

|---|---|

| April to February | 7th of the following month |

| March | 30th April (extended deadline) |

Example: TDS deducted in July must be deposited by 7th August. TDS deducted in March must be deposited by 30th April.

The deposit is made using Challan ITNS 281 on the Income Tax portal or through authorised bank branches.

TDS Return Filing Under Section 194I

Businesses and firms deducting TDS under Section 194I must file quarterly TDS returns in Form 26Q.

| Quarter | Period | Due Date |

|---|---|---|

| Q1 | April – June | 31st July |

| Q2 | July – September | 31st October |

| Q3 | October – December | 31st January |

| Q4 | January – March | 31st May |

After filing the return, the deductor must issue Form 16A (TDS certificate) to the landlord within 15 days of the due date for filing the TDS return. The landlord uses this certificate to claim TDS credit while filing their ITR.

What Is Section 194IB — TDS on Rent by Individuals?

As mentioned earlier, individuals and HUFs who are not subject to tax audit are exempt from Section 194I. However, Section 194IB was introduced to cover high-rent payments made by such individuals.

Under Section 194IB:

- Who must deduct: Individual or HUF tenants (not covered under 194I)

- Threshold: Monthly rent exceeds ₹50,000

- TDS rate: 5%

- When to deduct: At the time of paying rent for the last month of the tenancy or the last month of the financial year — whichever is earlier (i.e., once a year, not monthly)

- TDS return: File Form 26QC (not Form 26Q)

- TDS certificate: Issue Form 16C to the landlord

Important: Under Section 194IB, TDS is deducted only once — at year-end or when the tenancy ends — not every month. This makes it simpler for individual tenants.

Example: Rahul pays ₹60,000/month rent for his office. Since his business is not subject to tax audit, Section 194I does not apply. But Section 194IB does. He must deduct 5% TDS (i.e., ₹3,000) on one month's rent at year-end and deposit it using Form 26QC within 30 days.

Section 194I vs Section 194IB — Quick Comparison

| Feature | Section 194I | Section 194IB |

|---|---|---|

| Who deducts | Companies, firms, audit-required individuals/HUFs | Individuals/HUFs not under audit |

| Threshold | ₹2,40,000 per year | ₹50,000 per month |

| TDS rate | 10% (land/building) or 2% (machinery) | 5% |

| Frequency | Monthly (as rent is credited/paid) | Once a year (at year-end or lease end) |

| TDS return | Form 26Q | Form 26QC |

| TDS certificate | Form 16A | Form 16C |

How Does a Landlord Claim TDS Credit?

When a tenant deducts TDS on rent, the amount is reflected in the landlord's Form 26AS and Annual Information Statement (AIS). The landlord:

- Declares the gross rental income in their ITR under "Income from House Property" or "Business Income" (if commercial)

- Claims TDS credit for the amount already deducted by the tenant

- The net tax payable reduces accordingly

Example: Gross annual rent = ₹5,00,000. TDS deducted by tenant at 10% = ₹50,000. Landlord declares ₹5,00,000 as income but gets credit for ₹50,000 already paid as TDS. Only the remaining tax (if any, after deductions) needs to be paid.

Consequences of Not Deducting or Depositing TDS

Failing to comply with Section 194I has serious consequences:

Interest under Section 201(1A)

- 1% per month if TDS was not deducted at all

- 1.5% per month if TDS was deducted but not deposited with the government

Penalty under Section 271C

A penalty equal to the amount of TDS not deducted or deposited may be levied.

Disallowance of rent expense under Section 40(a)(ia)

If TDS is not deducted on rent, 30% of the rent paid is disallowed as a business expense while computing taxable income. This means you pay tax on income you never earned — a costly mistake.

Prosecution under Section 276B

In extreme cases, wilful non-deposit of TDS can lead to imprisonment of 3 months to 7 years.

Practical Tips for Tenants

- Get the landlord's PAN before making the first payment. Without PAN, you must deduct TDS at 20%.

- Set a calendar reminder for TDS deposit due dates — the 7th of every month for rent paid the previous month.

- Do not deduct TDS on the GST component. If the landlord charges GST on rent, TDS under Section 194I applies only on the base rent amount, not on the GST portion.

- Keep Form 16A ready. File your TDS return on time and issue Form 16A to the landlord quarterly — this avoids disputes.

- Check if rent agreement specifies gross or net rent. Some agreements mention rent inclusive of TDS — confirm with your CA how to handle this.

Frequently Asked Questions

Q: Is TDS on rent applicable on residential property rented for personal use? If you are an individual or HUF not subject to tax audit and you pay ₹50,000 or less per month, no TDS applies. If monthly rent exceeds ₹50,000, Section 194IB applies at 5%.

Q: Does TDS apply if the landlord is a company or trust? Yes. TDS under Section 194I applies regardless of whether the landlord is an individual, company, trust, or any other entity — as long as the threshold is crossed and the tenant is covered.

Q: What if the property has multiple owners (joint landlords)? TDS is deducted on the total rent paid. If the threshold is crossed on the aggregate amount, deduct TDS and issue separate Form 16A to each co-owner in proportion to their share.

Q: Is TDS on rent applicable on a co-working space subscription? It depends on the nature of the arrangement. If the payment is for a dedicated space under a lease agreement, it qualifies as rent. If it is a service fee for a flexible desk, it may be treated as a service payment under other TDS sections. Consult a CA for the specific arrangement.

Q: Can the landlord request no TDS deduction by submitting Form 15G or 15H? No. Form 15G and 15H are only applicable for interest income (Section 193/194A). There is no provision for a landlord to submit a declaration to avoid TDS under Section 194I. The landlord must declare the income and claim credit in their ITR.

Conclusion

TDS on rent under Section 194I is a straightforward but often overlooked compliance requirement for businesses, firms, and individuals who pay significant rent. Whether you are a company paying for your office premises or an individual renting out a commercial space, understanding these rules protects you from penalties, disallowances, and notices.

The key takeaways:

- Tenants covered under Section 194I must deduct 10% TDS on land/building rent above ₹2,40,000 per year

- Individual tenants paying more than ₹50,000/month must deduct 5% TDS under Section 194IB

- Always get the landlord's PAN — missing PAN means 20% TDS

- Deposit TDS by the 7th of the following month

- File Form 26Q quarterly and issue Form 16A to the landlord

- Non-compliance leads to interest, penalties, and 30% disallowance of rent expense

When in doubt, consult a chartered accountant to ensure your rent payments are TDS-compliant from day one.