Accounting is the backbone of every business. Whether you're a business owner, accounting student, entrepreneur, or finance professional, understanding the Golden Rules of Accounting is essential for maintaining accurate financial records. These rules form the foundation of the double-entry bookkeeping system and help determine which account should be debited and which should be credited in every transaction. In this guide, we'll explain the three Golden Rules of Accounting with practical examples.

What Are the Golden Rules of Accounting?

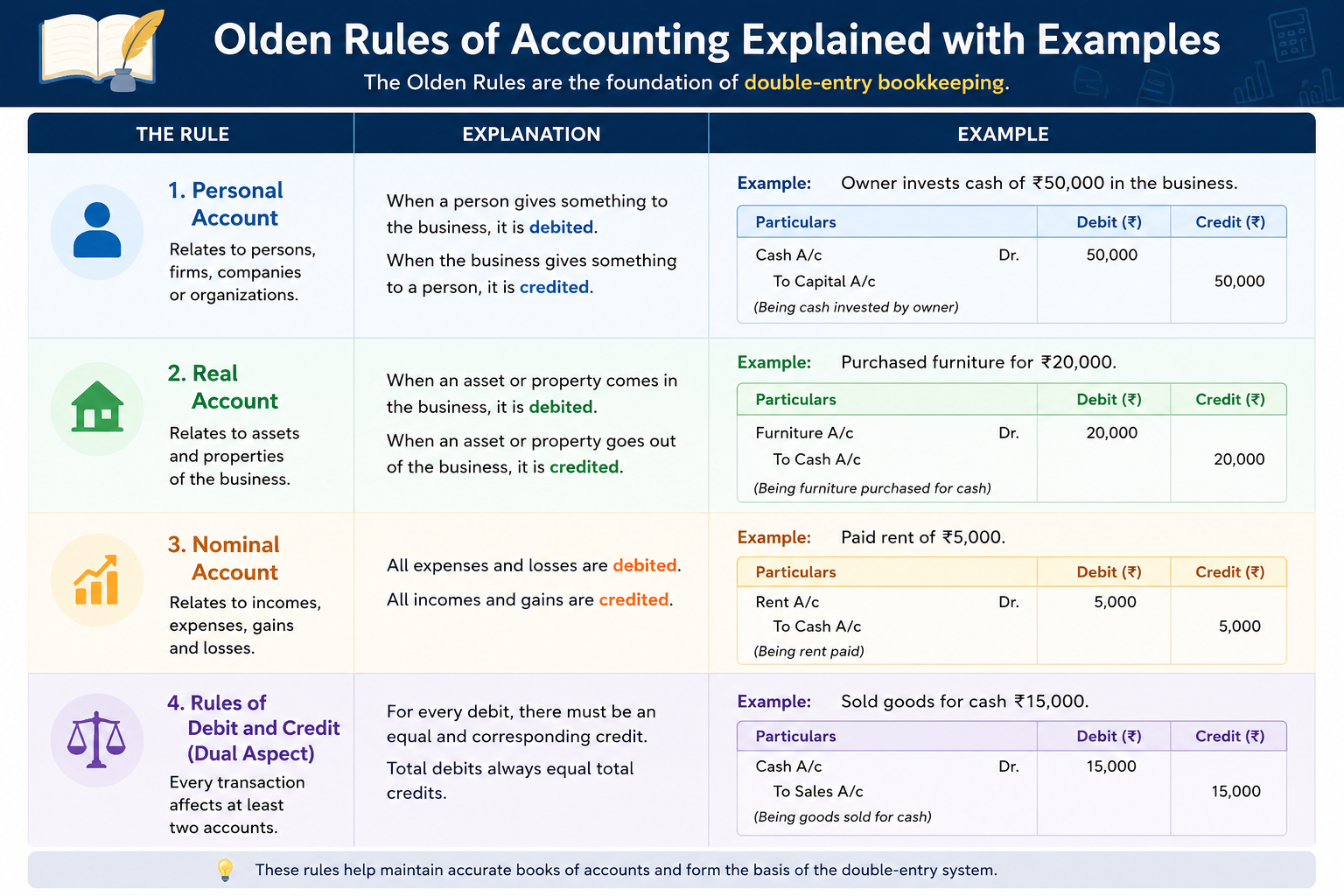

The Golden Rules of Accounting are principles used to record financial transactions correctly. Every accounting transaction affects at least two accounts, and these rules help identify the appropriate debit and credit treatment.

The three Golden Rules are:

- Personal Account

- Real Account

- Nominal Account

Let's understand each rule in detail.

1. Personal Account

Rule:

Debit the Receiver, Credit the Giver

A Personal Account relates to individuals, companies, firms, banks, or other organizations.

Examples of Personal Accounts

- Customer Accounts

- Supplier Accounts

- Bank Accounts

- Owner's Capital Account

- Creditor Accounts

Example 1

Mr. Sharma pays ₹20,000 to the business.

Journal Entry:

Bank A/c Dr. ₹20,000

To Mr. Sharma A/c ₹20,000

Explanation:

- Bank receives money → Debit

- Mr. Sharma gives money → Credit

Example 2

Business pays ₹10,000 to a supplier.

Supplier A/c Dr. ₹10,000

To Bank A/c ₹10,000

Explanation:

- Supplier receives payment → Debit

- Bank gives payment → Credit

2. Real Account

Rule:

Debit What Comes In, Credit What Goes Out

A Real Account relates to tangible and intangible assets owned by the business.

Examples of Real Accounts

- Cash

- Furniture

- Building

- Machinery

- Land

- Computer Equipment

- Patents

- Trademark

Example 1

Furniture purchased for ₹50,000 in cash.

Journal Entry:

Furniture A/c Dr. ₹50,000

To Cash A/c ₹50,000

Explanation:

- Furniture comes into the business → Debit

- Cash goes out → Credit

Example 2

Machinery sold for ₹1,00,000.

Journal Entry:

Cash A/c Dr. ₹1,00,000

To Machinery A/c ₹1,00,000

Explanation:

- Cash comes in → Debit

- Machinery goes out → Credit

3. Nominal Account

Rule:

Debit All Expenses and Losses, Credit All Incomes and Gains

Nominal Accounts relate to expenses, losses, incomes, and gains of a business.

Examples of Nominal Accounts

- Salary Expense

- Rent Expense

- Electricity Expense

- Interest Income

- Commission Received

- Discount Received

Example 1

Salary paid ₹30,000.

Journal Entry:

Salary A/c Dr. ₹30,000

To Cash A/c ₹30,000

Explanation:

- Salary is an expense → Debit

- Cash goes out → Credit

Example 2

Commission received ₹15,000.

Journal Entry:

Cash A/c Dr. ₹15,000

To Commission Received A/c ₹15,000

Explanation:

- Cash comes in → Debit

- Commission is income → Credit

Quick Summary of Golden Rules

| Account Type | Golden Rule |

|---|---|

| Personal Account | Debit the Receiver, Credit the Giver |

| Real Account | Debit What Comes In, Credit What Goes Out |

| Nominal Account | Debit All Expenses & Losses, Credit All Incomes & Gains |

Why Are Golden Rules of Accounting Important?

Understanding these rules helps businesses:

- Maintain accurate financial records

- Prepare reliable financial statements

- Reduce accounting errors

- Improve compliance and auditing processes

- Make informed business decisions

- Simplify bookkeeping and tax filing

Whether you're managing a startup, a small business, or a large enterprise, these accounting principles remain fundamental to financial management.

Common Mistakes to Avoid

- Confusing personal and real accounts

- Recording expenses as assets

- Incorrect debit and credit entries

- Ignoring supporting documents

- Not reconciling accounts regularly

Regular bookkeeping reviews can help prevent these errors and ensure compliance with accounting standards.

Conclusion

The Golden Rules of Accounting are the foundation of every financial transaction. By understanding Debit the Receiver, Credit the Giver, Debit What Comes In, Credit What Goes Out, and Debit All Expenses and Losses, Credit All Incomes and Gains, businesses can maintain accurate books and make better financial decisions.

If you need professional assistance with bookkeeping, accounting, GST compliance, tax filing, or financial reporting, consulting an experienced Chartered Accountant can help ensure accuracy and compliance.

Need Help With Accounting & Tax Compliance?

Our team provides:

✔ Bookkeeping Services

✔ GST Registration & Filing

✔ Income Tax Return Filing

✔ Company Registration

✔ ROC Compliance

✔ Financial Reporting & Advisory

Contact us today for professional accounting and tax solutions.