Managing multiple branches across different states? Then understanding GST on branch-to-branch transfers is essential for staying compliant and avoiding tax notices. Many businesses assume that moving goods between their own branches is not taxable; however, under GST, this is not always the case. In this guide, we explain when GST applies to branch transfers, valuation rules, ITC impact, compliance requirements, and common mistakes to avoid.

What Is a Branch-to-Branch Transfer Under GST?

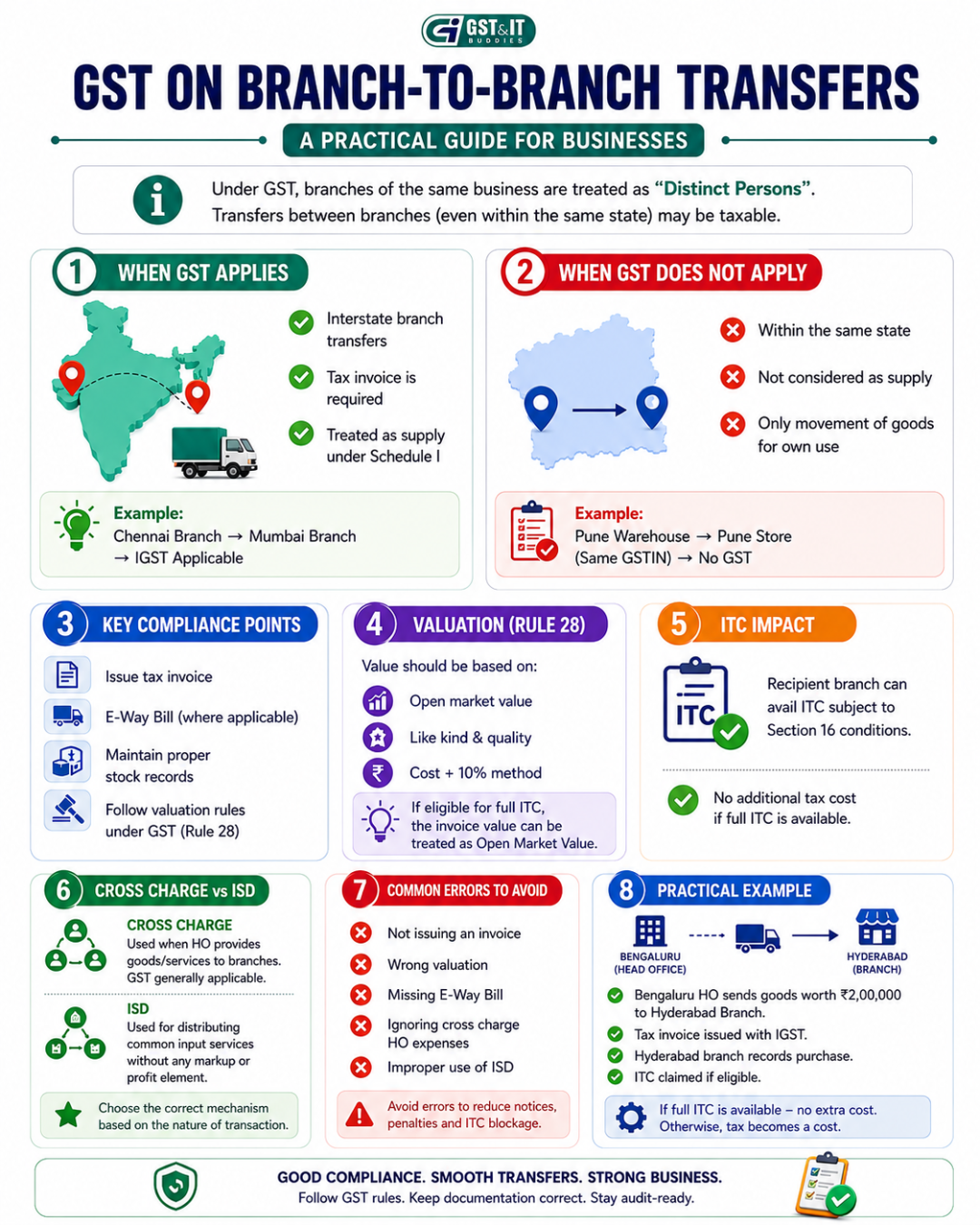

A branch-to-branch transfer refers to the movement of goods or services between different branches of the same business.

Example: The

- The Head Office in Delhi is sending stock to the Gujarat Branch

- Warehouse in Jaipur is transferring goods to the Mumbai Office

Under the GST law, branches registered in different states are treated as “Distinct Persons”, even if they belong to the same PAN.

This means certain transfers between branches become taxable transactions.

When Does GST Apply to Branch Transfers?

1. Interstate Branch Transfer (GST Applicable)

If goods are transferred between branches located in different states, GST applies.

Example:

A Delhi branch sends goods to a Gujarat branch.

✅ GST Applicable

✅ IGST will be charged

✅ Tax invoice is mandatory

This transfer is treated as a supply under Schedule I of GST, even if there is no sale involved.

Why Is GST Charged?

Because under GST, branches with separate registrations are considered separate taxable persons.

So even though ownership remains the same, tax still applies.

When GST Does NOT Apply

2. Transfer Within Same State (Same GSTIN)

If stock moves between locations under the same GST registration, GST generally does not apply.

Example:

A Jaipur warehouse transfers inventory to a Jaipur retail outlet under the same GSTIN.

✅ No GST charged

✅ Not treated as supply

✅ Only internal stock movement

However, businesses must maintain proper stock records for audit and reconciliation purposes.

Valuation of Branch Transfers Under GST (Rule 28)

A common question businesses ask:

“If there is no sale price, how is GST calculated?”

The answer lies in Rule 28 of GST Valuation Rules.

The value of branch transfer can be determined based on:

1. Open Market Value (OMV)

The price at which similar goods are sold in the market.

2. Like Kind and Quality

Value of similar products with comparable quality.

3. Cost + 10% Method

If market value is unavailable, the cost of production plus 10% margin may be used.

Important Rule:

If the receiving branch is eligible for full Input Tax Credit (ITC), the invoice value can generally be accepted as the deemed open market value.

This simplifies compliance for businesses.

Input Tax Credit (ITC) on Branch Transfers

The receiving branch can usually claim Input Tax Credit (ITC) on GST paid during transfer.

Example: The

Delhi branch transfers goods to the Gujarat branch and charges IGST.

- Delhi Branch → pays IGST

- Gujarat Branch → claims ITC

This ensures there is no additional tax burden, provided ITC eligibility conditions are met.

Compliance Requirements for Branch Transfers

Businesses must ensure proper documentation.

Key Compliance Checklist:

✔ Issue a Tax Invoice

✔ Generate E-Way Bill (where applicable)

✔ Maintain proper stock transfer records

✔ Follow valuation rules under Rule 28

✔ Reconcile transactions in GST returns

Missing these requirements may lead to notices or penalties.

Cross Charge vs ISD: What Businesses Should Know

Many companies confuse Cross Charge with Input Service Distributor (ISD).

Cross Charge

Used when a head office provides services to branches.

Example:

HO provides accounting or management support to branch offices.

GST generally applies.

ISD (Input Service Distributor)

Used to distribute common input tax credits without charging GST.

Example:

Software subscription used by all branches.

Understanding the difference is important during GST assessments.

Common Mistakes Businesses Make

Avoid these costly errors:

❌ No invoice for branch transfers

❌ Wrong valuation of goods

❌ Missing E-Way Bill

❌ Incorrect ITC claims

❌ Ignoring HO expense cross charge

❌ Improper use of ISD mechanism

These mistakes can trigger GST notices, penalties, or ITC reversal.

Practical Example of GST on Branch Transfer

Suppose:

A Jaipur Head Office transfers goods worth ₹1,00,000 to its Gujarat branch.

Since it is an interstate transfer:

- IGST will apply

- Tax invoice must be issued

- Gujarat branch can claim ITC

If ITC is fully available, there is usually no major tax cost impact.

Final Thoughts

Understanding GST on branch-to-branch transfers is crucial for businesses operating in multiple states.

The biggest rule to remember:

Different GST registrations = GST may apply, even without a sale.

By maintaining proper documentation, following Rule 28 valuation, and claiming ITC correctly, businesses can stay compliant and avoid unnecessary tax disputes.